Click the image to read the PDF

Click the button to download the PDF

Local Commentary

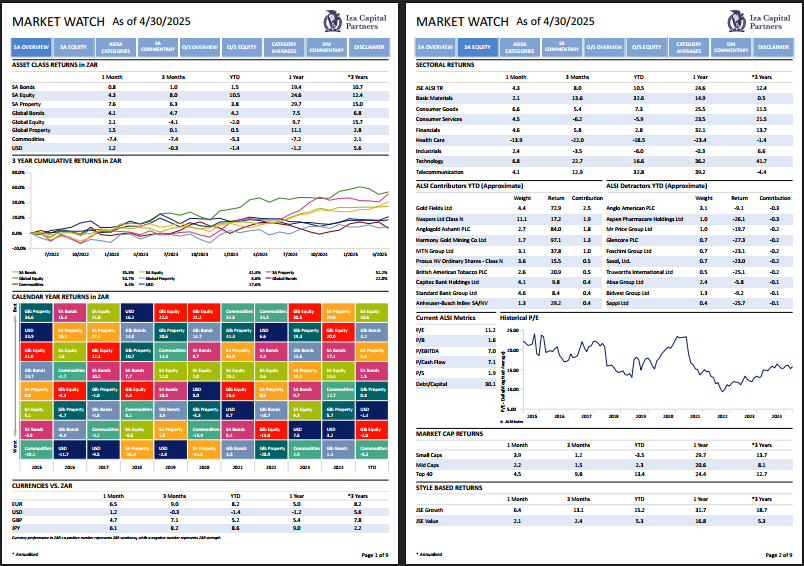

South African equity markets delivered another strong performance in April, with the FTSE/JSE All Share Index advancing 4.3% for the month, capping a robust start to the second quarter. However, this positive result belied significant volatility during the month, as investors initially grappled with global trade tensions and domestic political uncertainty.

April began with a steep sell-off, driven by news of sweeping U.S. trade tariffs that included 30% reciprocal duties on South African exports—an aggressive stance that rattled risk assets and saw the local bourse drop as much as 14% in early April. Global equity markets also experienced heightened volatility, with the MSCI Developed Market Index down 0.5% for the month and the S&P 500 posftng a 0.7% decline.

The recovery came swiftly, however, after the U.S. administration announced a 90-day delay on implementing the tariffs, opening the door to negotiations. South Africa’s diplomatic response was decisive: President Ramaphosa appointed Mcebisi Jonas, former deputy finance minister, as a special envoy to Washington to de-escalate tensions. This, along with domestic political concessions—including the withdrawal of a proposed 0.5% VAT increase—helped ease fears over government stability, bolstering investor confidence.

April’s rally was more balanced than previous months. While gold stocks again contributed meaningfully thanks to a 5% surge in the gold price (taking YTD gains to over 23%), gains were more widely distributed.

Retailer Clicks gained 17% in April after reporting upbeat interim results. Revenue rose 8.3% year-on-year, earnings per share grew 13%, and management guided for continued expansion with an increase in pharmacy and store rollouts for the rest of the year. Financials also performed strongly—Capitec rose 11% after reporting 30% growth in FY25 headline earnings, underscoring its ability to capture market share in a difficult environment.

On the downside, Aspen fell sharply (-25%) after disclosing that a dispute at its French production facility could halve earnings. Platinum miners also underperformed, dragged lower by softer PGM prices, underscoring the volatility and commodity-specific risks in the resources sector.

SA listed property experienced a rollercoaster month, dropping 5.6% in the first week before rebounding to finish up 7.6% for April. The rebound was driven by strong operational updates across the sector. Investors were encouraged by improved earnings visibility, high payout ratios, and renewed confidence in the sector’s ability to withstand policy and rate shocks.

The local bond market was initially hit by rising fiscal concerns, particularly at the longer end of the curve. While SA 10-year yields briefly breached 11% intra-month, they settled at 10.6% by month-end—unchanged from March. Bond performance recovered into month-end, with the ALBI index returning +0.8%. Short-dated bonds outperformed, supported by declining inflation and a growing consensus that rate cuts are likely in the second half of 2025.

The inflation backdrop remains benign. Headline inflation for March (reported in April) slowed to 2.7%—well below consensus and the third-lowest reading in over two decades. Core CPI also surprised to the downside at 3.1%. Key contributors included lower services inflation, falling education inflation, and subdued fuel prices. With the VAT hike scrapped, inflation is expected to remain below 3% for the next two months before trending toward the SARB’s 4.5% midpoint target.

Given these trends, market participants are increasingly pricing in a 50bps rate cut by year-end, with the first 25bps move anticipated as early as the May MPC meeting. While the SARB has maintained a hawkish tone—citing risks from the weak rand and external volatility—the data increasingly supports a less restrictive policy stance.

In contrast to the broad rally in local assets, the rand weakened by 1.5% against the U.S. dollar in April. This bucked the trend among emerging markets, where most currencies strengthened on the back of a broadly weaker dollar. Persistent concerns about domestic political cohesion and diplomatic tensions with the U.S. weighed on the currency. Still, the rand remains 1.4% stronger year-to-date, offering some buffer against imported inflation.

Growth data released in April continued to disappoint. Retail sales momentum has faded following the “two-pot” pension boost earlier in the year, while manufacturing and mining output also softened. The IMF revised South Africa’s GDP forecast downward, now expecting 1% growth for 2025. On the bright side, the transport sector showed signs of recovery, potentially contributing positively to Q1 GDP. Nevertheless, the balance of data suggests the SARB may need to recalibrate its stance if it hopes to support a sputtering economy.

Looking Ahead

April’s market dynamics underscored how quickly sentiment can shift. From tariff panic to a broad-based rebound, investors were reminded of the value of staying diversified and avoiding knee-jerk reactions. While geopolitical and fiscal risks remain elevated, the disinflationary environment, improving bond market dynamics, and earnings resilience across parts of the equity market provide a foundation for cautious optimism.

Our outlook remains grounded in valuation discipline, with an emphasis on real returns and downside protection.

Offshore Commentary

Policy Uncertainty Pushes Volatility to Historic Levels

April 2025 delivered a stark reminder of how deeply policy uncertainty can ripple through global financial markets. The month began with an aggressive salvo of trade measures from the U.S. administration, reigniting fears of a full-scale trade war. The resulting market turmoil was immediate and severe, triggering the largest two-day value decline in equity market history. The S&P 500 fell by 10.5% over just two trading sessions, a drop that now ranks among the steepest in the index’s history, rivaling even the worst days of the 2008 financial crisis and the 2020 pandemic shock.

Investor anxiety surged as President Trump unveiled sweeping tariffs that exceeded market expectations, targeting sectors critical to global supply chains. The market’s reaction was switi, with the VIX, a key measure of implied volatility, spiking to 60, a level not seen since the onset of COVID-19. This “Trump Thump,” as dubbed by financial media, wiped out nearly $1.1 trillion in market capitalization in just 48 hours.

Equity Markets, From Freefall to Recovery

After the initial rout, markets saw a sharp reversal mid-month as the U.S. administration moderated its stance, announcing a 90-day pause on some tariffs and exemptions for key electronics components. The geopolitical tone sotiened further, particularly toward China, with signals of renewed diplomatic dialogue. These developments triggered a dramatic rebound in equities, with the S&P 500 posting its strongest eight-day gain since November 2020, up nearly 12% from its monthly low.

Despite this volatility, developed market equities ended the month up 0.9%. However, U.S. stocks lagged most of their global counterparts. Growth stocks, particularly in technology, outperformed value stocks, with the energy sector notably dragging on performance due to falling oil prices. Emerging markets held up relatively well, supported by strong returns in Brazil and Mexico, countries perceived as less exposed to U.S. trade penalties.

Fixed Income, Yields Swing with Policy and Growth Signals

Bond markets were no less volatile. U.S. Treasury yields initially surged, with the 10-year peaking at 4.6% on April 11 as fears of inflation and economic instability took hold. But yields quickly retreated to 4.2% by month-end as risk sentiment improved and inflation data came in sotier than expected. March inflation figures showed headline CPI at 2.4% and core at 2.8%, both below consensus estimates, increasing the likelihood of rate cuts later this year.

In the eurozone, the European Central Bank reduced the deposit rate by 25 basis points to 2.25%, citing that disinflation was “well on track” and acknowledging a deteriorating outlook due to trade headwinds. Falling eurozone bond yields helped push global aggregate bond indices into positive territory, further buoyed by strength in the euro and yen against the U.S. dollar.

UK gilt yields were highly volatile but ended lower, driven by a cooling in March inflation and weaker economic data. The Bank of England is now widely expected to cut rates in May.

Credit markets were also rocked by the policy shock, with spreads widening sharply in the wake of the tariff announcements. However, much of the riskoff move was later reversed as investor confidence rebounded. Higher-quality credit demonstrated notable resilience, supported by cleaner balance sheets and deleveraging efforts across the corporate sector in recent years.

Commodities and Alternatives, Divergent Reactions to Uncertainty

Gold emerged as the standout beneficiary of April’s upheaval, rallying to a record high of $3,500 per ounce on April 22. The rally reflected both safe-haven demand and rising expectations of central bank easing. In contrast, oil prices fell 16% during the month amid rising recession fears and a decision by OPEC + to raise output, catching many investors off guard. Industrial metals also weakened as demand expectations slumped.

Macro Backdrop, Global Signals of Slowing Momentum

United States

Signs of economic sotiening were evident. The flash composite PMI fell to 51.2, led by a deceleration in services (51.4), while manufacturing ticked up to 50.7. Business expectations and consumer sentiment measured by the University of Michigan fell to pandemic-era lows. These metrics underscore how confidence shocks, driven by erratic policy moves, can disrupt investment and spending decisions and raise the risk of a recession. The S&P 500 closed the month down 0.7%, underperforming other developed markets. Energy and healthcare stocks were among the worst-performing sectors.

Europe and the UK

In the eurozone, the composite PMI declined to 50.1, with services contracting at 49.7. Manufacturing, while stable at 48.7, faced challenges from U.S. tariffs, which included a 25% levy on autos. However, lower energy prices and anticipated fiscal support helped cushion the blow. The EU’s suspension of retaliatory tariffs on U.S. steel and aluminum, combined with political stability in Germany, brought some relief. European equities ended the month slightly lower, down 0.4%.

In the UK, economic indicators pointed to contraction. The composite PMI fell to 48.2, with both trade uncertainty and domestic fiscal tightening weighing on activity. UK equities declined by 0.2% in April.